An Exclusive Financial Analysis of Global IME Bank

August 12, 2019 | Investopaper

Introduction of Global IME Bank

Establishment:

Global Bank Limited (GBL) was established in 2007. It was established as an ‘A’ class commercial bank in Nepal. The initial capital size of the bank stood at Rs. 1 billion. Now, the paid-up capital of the bank has increased to Rs. 10.31 billion. Global IME Bank (GBIME) is the success story of merger/acquisition in the banking sector of Nepal. It is the bank that set the trend of mergers in the Nepalese banking system.

Related: Financial Analysis of Commercial Banks of Nepal [With Ranking]

Mergers/Acquisitions:

Global IME Bank (GBIME) was formed after the merger of Global Bank with IME Financial Institution and Lord Buddha Finance in 2012. Both the IME Finance and Lord Buddha Finance were “C” class finance companies of Nepal. After that, Global IME Bank (GBIME) merged two more development banks in 2013. They were Social Development Bank and Gulmi Bikas Bank. Both the institution were “B” class development banks. In 2014, the mergers continued. Global IME Bank (GBIME) took Commertz and Trust Bank Nepal as the merger partner. It was the first time Global IME Bank (GBIME) merged with an “A” class commercial bank. Likewise, in the period between 2015 and 2016, GBIME acquired two “B” class Development Banks. Namely Pacific Development Bank and Reliable Development Bank.

Currently, the bank has signed an acquisition agreement with Hathway finance (“C” class finance). Also, Global IME Bank (GBIME) is also in the merger process with Janata Bank Nepal. Janata Bank Nepal is an “A” class commercial bank of Nepal.

Related: Merger/Acquisition By Commercial Banks In Nepal

Promoters:

The bank has a well renowned and respected businessman of Nepal as its promoters. The promoters come from a variety of different sectors such as finance, remittance, trading, export, automotive services, manufacturing, media services, and hydropower. The bank is led by a leading entrepreneur of Nepal, Mr. Chandra Prasad Dhakal. He is the Executive Chairman of IME Group of Companies. It is one of the fastest-growing business conglomerates in Nepal. It has a presence in banking, money service, IT, trading, hydro-energy, travel and tourism, cable car and infrastructures.

Recognition:

Global IME Bank (GBIME) received “The Bank of the Year Award 2014” for Nepal. It was provided by the Bankers Magazine published by the Financial Times of UK. Similarly, International Finance Magazine (London) presented GBIME with “Best Internet Bank 2016- Nepal”. Likewise, World HRD Congress (India) provided GBIME with the “Best Employer Award 2018″.

Expansion:

Global IME Bank (GBIME) has an ever-expanding customer base of more than 10 lakh accounts in deposits. Likewise, the credit accounts stand at above 24 thousand. The bank has established the provincial office in all seven provinces, as directed by the Nepal Rastra bank. GBIME provides services to its customers through:

—142 branches

—7 extension counter

—15 Revenue Collection counter

—1 CDS & Clearing Counter

—115 Branchless Banking services

—141 ATMs

Board of directors of Global IME Bank

The board of directors of GBIME includes 7 members. Mr. Chandra Prasad Dhakal leads the board as the chairman. The board of directors of Global IME Bank includes:

| S.N. | Board Members | Post | Representative |

| 1 | Chandra Prasad Dhakal | Chairman | Promoter shareholders |

| 2 | Pawan Kumar Bhimsariya | Director | Promoter shareholders |

| 3 | Sudharshan Krishna Shrestha | Director | Ordinary Shareholders |

| 4 | Suman Pokharel | Director | Ordinary Shareholders |

| 5 | Krishna Prasad Sharma | Director | Ordinary Shareholders |

| 6 | Numnath Poudel | Director | Independent |

| 7 | Bishnu Prasad Baskota | Company Secretary |

Management team of Global IME Bank

After the resignation of Mr. Janak Sharma Paudyal, the bank is led by Mr. Mahesh Sharma Dhakal. He is the Acting Chief Executive Officer of the Bank. The other team members in the management committee are:

| S.N. | Management Team | Post |

| 1 | Mr. Mahesh Sharma Dhakal | Acting Chief Executive Officer |

| 2 | Mr. Surendra Raj Regmi | Assistant General Manager |

| 3 | Ms. Arati Rana | Assistant General Manager |

| 4 | Mr. Bhawani Dhakal | Chief Compliance Officer |

| 5 | Mr. Anil Joshi | Head – Information Technology/Card & E-banking |

| 6 | Mr. Buddhi Akela | Chief Risk Officer |

| 7 | Mr. Raja Aryal | Chief Financial Officer |

| 8 | Mr. Deep Chandra Regmi | Head – Human Resource |

| 9 | Mr. Ganesh Prasad Awasthi | Chief Operating Officer |

| 10 | Mr. Ranjan Kumar Thapa | Head – Treasury and International Banking |

Shareholding Structure of Global IME Bank

The bank is fully promoted by Nepalese investors. Almost 51.20 percent of total shares are owned by the promoters. Likewise, the general public has 48.80 percent ownership in the bank. Out of the promoter shareholders, institutions occupy 14.21 percent of the bank. Whereas, the individual promoters have 36.99 percent ownership in GBIME. The shareholding structure is shown in the table below:

| Ownership Structure | Percentage (%) |

| Domestic Ownership | 100 |

| Promoter (Institutions) | 14.21 |

| Promoter (Individual) | 36.99 |

| General Public | 48.8 |

| Foreign Ownership | – |

| Total | 100 |

Major Shareholders of Global IME Bank

IME Investment Pvt. Ltd. and Worldwide Investment Pvt. Ltd. possess 5.97 percent and 5.48 percent of the bank. The major shareholders of Global IME Bank (GBIME) with more than 1 percent share are shown in the table below:

| S.N. | Major Shareholders | Percent (%) |

| 1 | IME Investment Pvt. Ltd. | 5.97 |

| 2 | Worldwide Investment Pvt. Ltd. | 5.48 |

| 3 | Sumeet Kumar Agrawal | 2.94 |

| 4 | Uttam Kumar Nepal | 2.94 |

| 5 | Continental Investment Pvt. Ltd. | 2.82 |

| 6 | Usha Investment Pvt. Ltd. | 2.61 |

| 7 | Homeland Developers Pvt. Ltd. | 2.15 |

| 8 | Suraj Kumar Shrestha | 1.36 |

| 9 | Sandeep Agrawal | 1.33 |

| 10 | Hemraj Dhakal | 1.26 |

| 11 | Durga Prasad Neupane | 1.21 |

| 12 | Nimisa Investment Pvt. Ltd. | 1.02 |

Mergers and Acquisitions By Global IME Bank

Global IME Bank (GBIME) is the result of the merger/acquisition of 10 banking and financial institutions. In a way, it is a conglomerate in the banking sector of Nepal. The different mergers and acquisitions by the bank are shown in the table below:

| Institutions | Merger/Acquisition | Name after Merger/Acquisition | Year |

| Global Bank, IME Finance and Lord Buddha Finance | Merger | Global IME Bank | 2012 |

| Global IME Bank, Social Development Bank, Gulmi Bikas Bank | Merger | ” | 2013 |

| Global IME Bank, Commertz and Trust Bank | Merger | ” | 2014 |

| Global IME Bank, Pacific Development Bank, Reliable Development Bank | Acquisition | ” | 2015-16 |

| Global IME Bank, Hathaway Finance | Acquisition* | ” | 2019 |

| Global IME Bank, Janata Bank | Merger* | ” | 2019 |

Number of Employees, Branches, and ATMs of Global IME Bank

At present, the bank has more than 142 branches. Due to expansion as well as mergers/acquisitions, the branches and employees have grown at a steady pace. The bank had 1,700 employees until the end of fiscal year 2074/75. Likewise, the branches have increased from 84 in 2070/71 to 131 in 2074/75. Also, the ATMs have also grown in number from 84 to 134 during this period. The expansion of Global IME Bank (GBIME) in the last five years period is shown in the table below:

| Fiscal Year | Number of Employees | No. of Branches | Number of ATMs |

| 2070/71 | 1098 | 84 | 84 |

| 2071/72 | 1117 | 85 | 90 |

| 2072/73 | 1107 | 91 | 99 |

| 2073/74 | 1348 | 112 | 114 |

| 2074/75 | 1700 | 131 | 134 |

Financial Analysis of Global IME Bank: Last 5 Years

Paid-up Capital, Shareholders’ Fund and Total Assets

Global IME Bank (GBIME) has increased its capital by more than 2 times in the period between 2070/71 to 2075/76. The bank had a capital of Rs. 4.98 billion in the fiscal year 2070/71. This has grown to Rs. 10.31 billion at the end of the fiscal year 2074/75. Similarly, the shareholder’s fund has also doubled during this period. The fund which stood at Rs. 6.13 billion in 2070/71 has surged to Rs. 13.58 billion in the fiscal year 2074/75. Similarly, the total assets have also doubled to Rs. 125.85 billion. The total assets stood at Rs. 60.02 billion at the end of 2070/71.

The paid-up capital, shareholders’ fund and total assets of GBIME are shown in the table below:

| Fiscal Year | Paid-up Capital (Rs. ‘billion’) | Shareholder’s Fund (Rs. ‘billion’) | Total Assets (Rs. ‘billion’) |

| 2070/71 | 4.98 | 6.13 | 60.02 |

| 2071/72 | 6.16 | 7.32 | 69.19 |

| 2072/73 | 7.15 | 8.95 | 88.68 |

| 2073/74 | 8.89 | 12.37 | 117.89 |

| 2074/75 | 10.31 | 13.58 | 125.85 |

Paid-up capital of Global IME Bank(GBIME) in the last five years: In the chart

Deposits and Loans & Advances of Global IME Bank

The deposits of the bank stood at Rs. 106.51 billion at the end of the fiscal year 2074/75. In the year 2070/71, the total deposit collection was Rs. 52.29 billion. So, the deposits have more than doubled in a span of four years. Similarly, the total loans of the bank have grown to Rs. 93.37 billion at the end of 2074/75. The loans portfolio stood at Rs. 43.02 billion at the end of 2070/71. This indicates that the loans grew by almost 117 percent during this period. The growth in both the deposits and

The total deposits and loans of GBIME are shown in the table below:

| Fiscal Year | Deposits (Rs. ‘billion’) | Loans and Advances (Rs. ‘billion’) |

| 2070/71 | 52.29 | 43.02 |

| 2071/72 | 60.18 | 50.23 |

| 2072/73 | 74.68 | 60.84 |

| 2073/74 | 101.91 | 80.82 |

| 2074/75 | 106.51 | 93.37 |

Deposits and loans of Global IME Bank(GBIME) in the last five years: In the chart

Net Interest Income and Net Profit of Global IME Bank

GBIME earned a net interest income of Rs. 3.90 billion in the fiscal year 2074/75. This turned into Rs. 2.10 billion as the net profit for the year. Both the net interest income as well as net profit have increased by more than twofold in the four years. The net interest income grew from Rs. 1.76 billion in the fiscal year 2070/71. Likewise, the net profit has surged from 0.97 billion in 2070/71 to Rs. 2.10 billion in 2074/75.

Also Read: Net Profit of Commercial Banks in Nepal [With Ranking]

The net interest income and the net profit of GBIME are shown in the table below:

| Fiscal Year | Net Interest Income (Rs. ‘billion’) | Net Profit (Rs. ‘billion’) |

| 2070/71 | 1.76 | 0.97 |

| 2071/72 | 2.29 | 0.96 |

| 2072/73 | 2.89 | 1.38 |

| 2073/74 | 3.66 | 2.06 |

| 2074/75 | 3.9 | 2.1 |

Net Profit of Global IME Bank(GBIME) in the last five years: In the chart

Return On Equity (ROE) and Return On Assets (ROA)

Return On Equity (ROE) measures the profitability based on the shareholders’ equity. On the other hand, Return On Assets (ROA) measures the profit based on the total assets utilized to achieve the profit. So, both are good indicators for measuring the efficiency of the organization. GBIME has an average return on equity and capital in the past 5 years period. ROE stood between 13-28 percent whereas ROA remained in between 1.39 percent to 1.75 percent.

The return on equity (ROE) and return on assets (ROA) of GBIME are shown in the table below:

| Fiscal Year | Return on Equity (ROE %) | Return on Assets (ROA %) |

| 2070/71 | 16 | 1.62 |

| 2071/72 | 13 | 1.39 |

| 2072/73 | 16 | 1.58 |

| 2073/74 | 18 | 1.75 |

| 2074/75 | 15 | 1.67 |

Return On Equity (ROE) of Global IME Bank (GBIME) in the last five years: In the chart

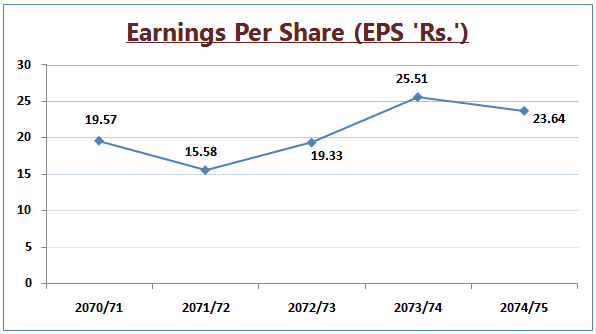

Earnings Per Share (EPS) and Networth Per Share

Earnings Per Share (EPS) and Networth Per Share are commonly used by investors while making investment decisions. EPS shows the per-share earnings while networth per share reflects the per-share book value. GBIME has EPS of 23.64 as of fiscal year 2074/75. The EPS has remained relatively stable between 15 percent to 25 percent. Likewise, the net-worth per share has fluctuated between Rs. 118.83 to Rs. 139.15. At the end of the fiscal year 2074/75, the net-worth stood at Rs. 131.72.

The Earnings Per Share (EPS) and Networth Per Share of GBIME are shown in the table below:

| Fiscal Year | Earnings Per Share (EPS ‘Rs.’) | Networth Per Share (‘Rs.’) |

| 2070/71 | 19.57 | 123.09 |

| 2071/72 | 15.58 | 118.83 |

| 2072/73 | 19.33 | 125.17 |

| 2073/74 | 25.51 | 139.15 |

| 2074/75 | 23.64 | 131.72 |

Earnings Per Share (EPS) of Global IME Bank(GBIME) in the last five years: In the chart

Non-Performing Loans (NPL) and CCD Ratio

The bank has been able to reduce its NPL gradually. The NPL stood at 2.55 percent in the fiscal year 2070/71. However, it has steadily declined to 0.77 percent at the end of the fiscal year 2074/75. Similarly, the bank has maintained the CCD ratio between 71.24 percent to 75.35 percent. CCD Ratio refers to the ratio of Credit to Core capital and deposits. It should be below 80 percent as directed by the central bank. At the end of the fiscal year 2074/75, the CCD ratio stood at 75.35 percent.

The non-performing loans (NPL) and CCD Ratio of GBIME are shown in the table below:

| Fiscal Year | Non-Performing Loans (NPL, %) | CCD Ratio (%) |

| 2070/71 | 2.55 | 73.64 |

| 2071/72 | 2.23 | 74.41 |

| 2072/73 | 1.89 | 72.69 |

| 2073/74 | 1.6 | 71.24 |

| 2074/75 | 0.77 | 75.35 |

Non-Performing Loans (NPL) of Global IME Bank(GBIME) in the last five years: In the chart

Dividend History of Global IME Bank

GBIME has consistently provided satisfactory dividends to the shareholders. For the increment of capital, the dividends are more focused towards the bonus share. The bank has distributed the dividend ranging from 16 percent to 25 percent in the past 5 years period. From the profit of the fiscal year 2074/75, the bank provided a 16 percent bonus share to the shareholders.

You May Also Like: Dividend History Of Commercial Banks Of Nepal

The dividend history of GBIME is shown in the table below:

| Fiscal Year | Bonus share (%) | Cash dividend (%) | Total dividend (%) |

| 2070/71 | 21 | 4 | 25 |

| 2071/72 | 23 | 0 | 23 |

| 2072/73 | 16 | 0 | 16 |

| 2073/74 | 10 | 10 | 20 |

| 2074/75 | 16 | 0 | 16 |

Total Dividend of Global IME Bank(GBIME) in the last five years: In the chart

Price History of Global IME Bank

For the full price history of GBIME, click on the link: Price History of Global IME Bank (GBIME)

Market Price and Market Capitalization of Global IME Bank

With the rise in the outstanding shares, the market price has declined gradually in the last 5 years. The share price was Rs. 640 at the end of 2070/71. However, it has fallen to Rs. 290 at the end of 2074/75. The crash of the stock market of Nepal is also the major reason for the decline in the share price of the bank.

The market capitalization of the Bank stood at Rs. 25.78 billion at the end of the fiscal year 2074/75. The bank has the highest market capitalization of Rs. 31.75 billion in the fiscal year 2072/73. After that period, the market value has fallen due to the crash of the stock market.

The market price and the market capitalization of GBIME are shown in the table below:

| Fiscal Year | Market Price Per Share (MPS ‘Rs’) | Market Capitalization (Rs. ‘billion’) |

| 2070/71 | 640 | 16.81 |

| 2071/72 | 479 | 14.05 |

| 2072/73 | 515 | 31.75 |

| 2073/74 | 388 | 28.1 |

| 2074/75 | 290 | 25.78 |

Market Capitalization of Global IME Bank(GBIME) in the last five years: In the chart

Financial Analysis of Global IME Bank: Fourth Quarter, 2075/76

The bank has shown a decent performance growth in the fourth quarter of the fiscal year 2075/76. The net profit has grown by more than 33 percent to Rs. 2.80 billion. To know about the fourth-quarter performance of the bank in 2075/76, click on the link below:

Global IME Bank (GBIME) Fourth Quarter Report

Conclusion

Global IME Bank (GBIME) is running in its 13 years in the Nepalese Banking industry. Although it is one of the newest banks, it has established itself as one of the leading banks of Nepal. The strategic merger and acquisition decisions have positioned the bank along with the likes of Everest and the Himalayan Bank which have completed more than 25 years in the banking industry. GBIME has always remained open to the merger and acquisition. It is currently in the merger process with Janata Bank. After the merger, GBIME will place itself as the largest commercial bank of Nepal. The bank will lead the industry in terms of major financial indicators such as capital size, deposit, loans, profit, etc.

Despite its merger successes, managing and motivating the employees will remain as the top challenge for the bank in the coming years. Likewise, to improve the profitability on the huge capital base and provide a decent return to the shareholders will also be a daunting task for the management. However, with the capable team, the bank can carry its past success into the future and emerge as the top bank of Nepal. Investors can expect satisfactory dividends in the future unless any unseen force comes into play.

NOTE: Figures of FY 2074/75 and FY 2073/74 are as per NFRS and the figures of the earlier year are as per previous GAAP. Hence, they may not be comparable.

(Investments are subject to market risks and investors are advised to do a personal homework before making any investment decision. This material is just a guideline for the investors to do further investigations)

Read Related Contents:

Financial Analysis of Nabil Bank Limited

Global IME Bank Ltd. and Global IME Bank Ltd. Promoter Share both are found listed in NEPSE. ]

Could you please clarify the difference between these two?

This information has helped me in research report related to capital structure and its impact on banks profitability of GIBL for bbs forth year..thank u GIBL