Nepal Investment Bank: A brief Company Analysis

January 6 , 2019 | Investopaper

The brief company analysis of Nepal Investment bank as performed by Investopaper team in 2075 is as follows:

Introduction

Nepal Investment Bank Ltd. (NIBL), previously Nepal Indosuez Bank Ltd., was established in 1986 as a joint venture between Nepalese and French partners. The French partner (holding 50% of the capital of NIBL) was Credit Agricole Indosuez, a subsidiary of one of the largest banking groups in the world.

Later, in 2002 a group of Nepalese companies comprising of bankers, professionals, industrialists, and businessmen acquired the 50% shareholding of Credit Agricole Indosuez in Nepal Indosuez Bank Ltd., and accordingly, the name of the Bank also changed to Nepal Investment Bank Ltd.

You May Also Like: Financial Analysis of Commercial Banks of Nepal

Board of directors and the Management team of Nepal Investment Bank:

The board of directors includes:

The management of Nepal Investment Bank is led by Mr. Jyoti Prakash Pandey. The management team includes:

Financial Highlights of Nepal Investment Bank: Last 5 Years

-

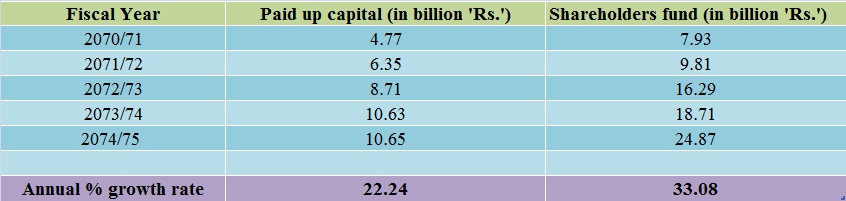

Paid-up capital & Shareholders fund:

The current paid-up capital of the bank stands at Rs. 10.65 Arab. After an 18% bonus share adjustment this year, the paid-up capital will reach Rs.12.57 Arab. The capital has increased in the past four years by 22.24% annually. NIBL has consistently increased the capital by providing good bonus shares to the shareholders. The Further Public Offering (FPO) and acquisition of Ace Development Bank has also strengthened the capital and reserve of the bank.

The bank has satisfactory growth in shareholders’ fund. The shareholders’ fund has risen by 33.08% annually in the past 4 years. The shareholders’ fund as of Ashad end, 2075 stands at Rs. 24.87 Arab which is comparatively better than other banks.

-

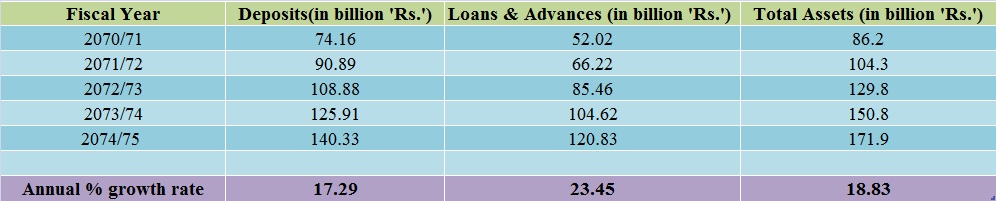

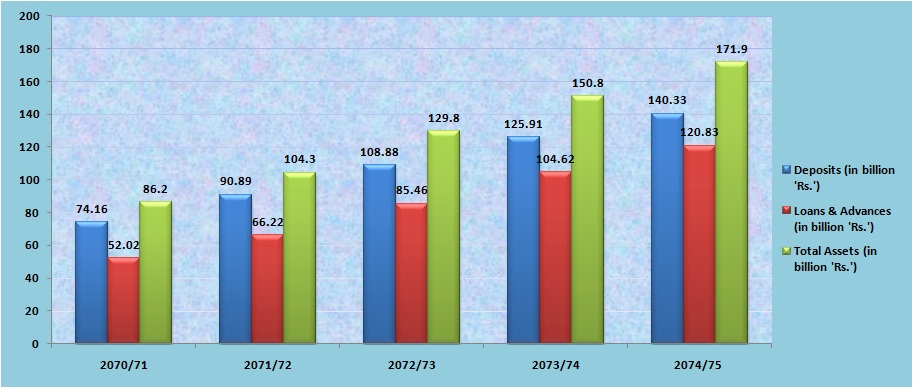

Deposits,loans & total assets:

Deposits and loans have moderately increased in the past five years. The bank has grown the deposits by 17.29% and increase its loan portfolio at 23.45 % annually in past 4 years. The deposits and loans stood at Rs. 140.33 Arab and Rs. 120.83 Arab at the end of Ashad 2075. The total assets of the bank have gradually increased by 18.83% annually to Rs. 171.9 Arab as of 2075. Nepal Investment Bank is one of the largest banks of Nepal in terms of assets size.

-

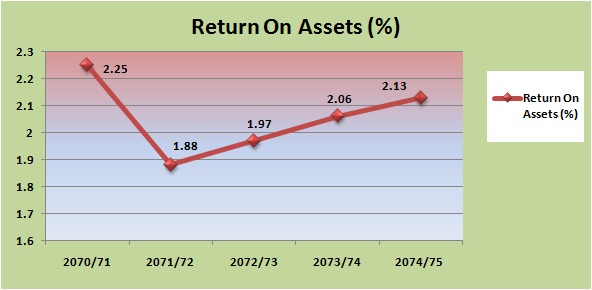

Return On Equity(ROE) & Return On Assets(ROA):

The ROE and ROA of the bank remain at 14.71 and 2.13 as of Ashad end 2075, which is an average return for the huge bank like NIBL. ROE is calculated based on closing equity. Hence its value is lower. The decrease in ROE is due to a huge increase in capital size. ROA, on the other hand, is gradually increasing in 4 years. This means that the bank is able to utilize its assets at an efficient rate of return.

-

EPS, MPS, BPS & P/E ratio:

The EPS and MPS reached a peak value of Rs. 40.67 and Rs. 1040 during the 5 years period. The EPS at the end of F.Y. 2075 stands at 35.66 while the market price is at 621. The P/E ratio is at 17.40 which is the lowest in five years. This means the bank price is at a cheaper level this year than in the past 5 years in relation to its earnings. Book value per share is at 236 which is the highest in five years.

-

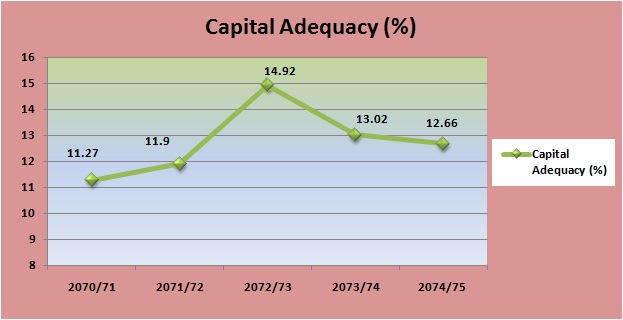

Capital Adequacy, Non-Performing Loans(NPL), Base rate :

The bank has maintained the capital adequacy level between 11% and 15% which is as per the NRB guidelines. The capital adequacy as of Ashad end 2075 stands at 12.66%.

The non-performing loan is at 1.36% at Ashad end, 2075. The non-performing loan has gradually increased in the last 3 years. This is due to the acquisition of the Ace development bank.

The base rate of the bank is 9.02 which is at the highest level in past 5 years. The high base rate is due to the increase in the cost of deposits and an increase in management expenses. The ongoing credit crisis in the entire banking industry has increased the cost of the overall banking sector.

-

Dividend History:

NIBL has provided satisfactory dividends to the shareholders ranging from 35% to 40%, in these five years. The bank declared an 18% bonus share & a 22% cash dividend this year.

You May Also Like: Dividend History Of Commercial Banks Of Nepal

-

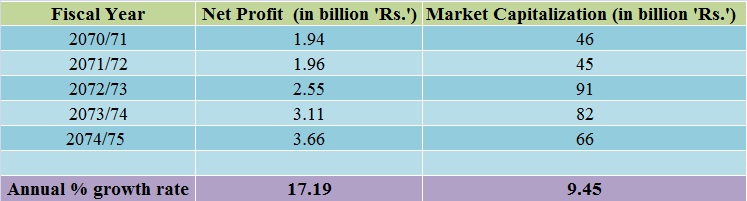

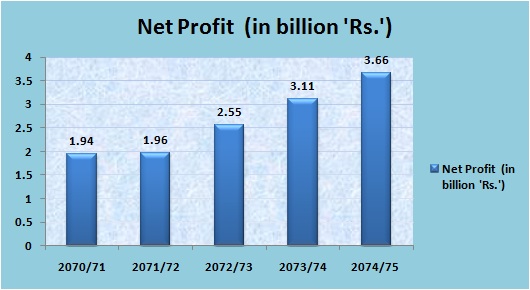

Net Profit & Market Capitalization:

Net Profit of Nepal Investment Bank has risen from Rs. 1.94 billion in 2070/71 to Rs.3.66 billion in 2074/75. The net profit has grown by satisfactory 17.19% annually.

Also Read: Net Profit of Commercial Banks in Nepal [With Ranking]

The market capitalization of NIBL has increased by a mere 9.45% annually. The bank was valued at Rs. 91 billion by the investors in 2072/73, the highest market valuation to date. In 2070/71, the market cap was 46 billion while in 2074/75, the market cap is at 66 billion. The market value of NIBL has not increased in this 5 years as much as the increase in net profit.

Financial Highlights of Nepal Investment Bank: 1st Qtr 2075/76

The 1st quarter of the current fiscal year for Nepal Investment Bank seems satisfactory. The deposits and loans grew by 7.56% & 17.32% from the previous year. Net profit also grew by 16.67%. Hence, EPS increased by 17.63% in first-quarter 2075/76. The ROE and ROA stand at 16.05 and 2.41%. The NPL increased by 16.35% to 1.21%. The base rate also increased slightly by 1.35% to 9.03.

Past investment returns of NIBL stock:

NIBL has provided healthy returns to the shareholders. The dividends have been quite satisfactory. Due to the overall market crash of more than 35%, the market value of the Nepal Investment Bank has not increased much during this period. However, considering four and half years investment horizon, NIBL shareholders earned at an annual rate of 10.67% in this period. As shown in the above table, if you had invested Rs.1,00,000 at the end of F.Y 2070/71 it would have generated the value worth Rs. 157,782 now. This is below average return for a blue-chip company like NIBL.

Future Prospects and challenges

Nepal Investment Bank is one of the leading commercial banks in Nepal. The board of directors and the management team of the company hold a high reputation. The management seems capable to grow the business and maintain the presence in the banking industry. Nepal Investment Bank has shown satisfactory results in the first three months in this fiscal year.

The high cost of doing business is, at current, the major challenge for the bank. For a leading commercial bank, a base rate at around 9% is quite high. The expansion of quality credit at a high-interest rate can be a problem for the bank. The growth rate of deposits is also shrinking. To increase the deposits while maintaining the lower cost of the fund at such competitive market seems to be a major challenge. The current credit crisis in the entire banking industry is also a major barrier to the bank.

The future of Nepal Investment Bank is dependent on the future of the banking industry. The interest rate plays a major role in the development of the banking sector. At the low-interest-rate environment, the banking and economic expansion is possible. In the capable hands of Prithvi Bahadur Pande, we can assume Nepal Investment Bank will continue to lead the entire banking industry in the future like it did in the past.

Decision

Nepal Investment Bank stock (NIB) has been the blue-chip stock for many years in Nepalese Share Market. It has provided good returns to the investors in the past as well as the present. The bank has always acted positively for the benefit of the shareholders. Net profit is gradually increasing with the increase in the size of Assets. However, the market valuation of the company has not increased much during this period. This is a plus point for the investor seeking value in their investment.

For the investor willing to invest in NIBL stock, we advise going for it. It is better to buy NIBL promoter at a cheaper price than NIBL ordinary since both are easily tradable. NIBL stock will provide balance to the investors’ portfolio by minimizing the risks. This is the stock to hold in the good market as well as bad. For dividend investors, NIBL can provide healthy income.

NOTE: Figures of FY 2074/75 are as per NFRS and the figures of the earlier year are as per previous GAAP. Hence, they may not be comparable.

(Investments are subject to market risks and investors are advised to do personal homework before taking any investment decision. This material is just a guideline for the investors to do further investigations)

Read Related Contents:

An Exclusive Financial Analysis of Global IME Bank

Financial Analysis of Himalayan Bank Limited