Sanima Bank: A brief company analysis

December 15, 2018 | Investopaper

The brief company analysis of Sanima bank as performed by Investopaper team is as follows:

Introduction

Sanima Bank Ltd. is one of the latest commercial banks in the Nepalese banking industry. It is promoted by prominent and dynamic Non-Resident Nepalese (NRNs) businessmen. It started its operation as a National level development bank in 2004. In 2012, the bank upgraded itself from a ‘B class’ development bank to ‘A-class’ commercial bank. It increased its paid-up capital from Rs. 80 crores to Rs.2 Arab by issuing 1:1.5 right shares and received the license from Nepal Rastra Bank to operate as a commercial bank. The bank’s head office is located at ‘Alakapuri’, Naxal.

Related: Financial Analysis of Commercial Banks of Nepal [With Ranking]

Board of directors and the Management Committee

The board of directors includes:

- Mr. Binaya Kumar Shrestha Chairman

- Mr. Tuk Prashad Poudel Director

- Mr. Shamba Lama Director

- Mr. Bharat Kumar Pokhrel Director

- Mr. Mahesh Ghimire Director

- Mr. Uttam Bhattarai Director

The management of Sanima bank is led by Bhuwan Dahal since 2014. The members of the management committee include:

- Bhuvan Kumar Dahal Chief Executive Officer

- Tej Bahadur Chand Deputy Chief Executive Officer

- Bobby Singh Gadtaula Chief Deposit Officer

- Nischal Raj Pandey Chief Risk Officer

- Pawan K Acharya Chief Project Financing Officer

- Saroj Guragain Chief Financing Officer

- Sujeet Dhakal Chief Retail Lending Officer

- Raju Krishna Shrestha Deputy Chief Operating Officer

Financial Highlights: Last 5 Years

- Paid-up capital:

The current paid-up capital stands at Rs. 8 Arab. The capital has increased in the past five years by 29.23% annually. The bank increased the capital to meet the minimum capital requirement enforced by Nepal Rastra Bank.

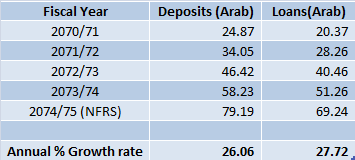

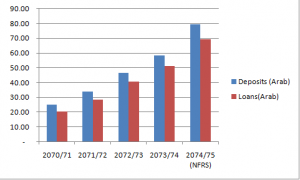

- Deposits and loans:

There has been a huge increment in deposits and loans in the past five years. The bank has been able to grow the deposits by 26.06% annually and increase its loan portfolio at 27.72 %. The deposits and loans stand at Rs. 79.19 and Rs. 69.24 at the end of Ashad 2075.

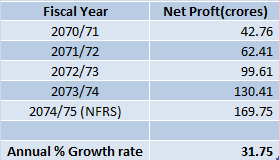

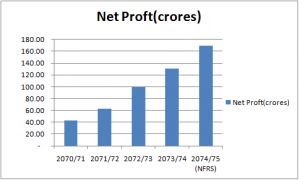

- Net profit:

The bank has been able to achieve outstanding growth in net profit. Net profit has risen by an impressive 31.75% annually but it is overshadowed by the fact that capital has increased by 29.23% annually in the past 5 years. The net profit as of Ashad end, 2075 stands at 169.75 crores.

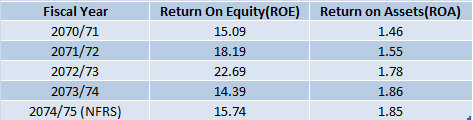

- Return On Equity(ROE) & Return On Assets(ROA):

The ROE and ROA of the bank remain at 15.74 and 1.85 which is an average return expected from banking institutions. The increase in profit did not satisfactorily improve the ROE and ROA due to additional capital injected into the bank to meet the capital requirement.

- EPS, MPS & P/E ratio:

The EPS and MPS reached a peak value of Rs. 32.55 and Rs. 750 on fiscal year 2072/73. The current EPS stands at 21.22 while the market price is at 324. The P/E ratio is at 15.27 which is the lowest in five years. This might indicate that the shares are currently available at a cheaper price to its earnings than it was in the past 5 years.

- Base rate and Non-Performing Loans(NPL):

The current base rate of the bank is 10.66 which is at the highest level in the past 5 years. The high base rate is due to the credit crunch in the entire banking industry. The intense competition between banks to collect deposits has pushed the cost of funds to a higher level. Also, there has been an increase in management expenses due to the expansion of branches. This has pushed the base rate up. The non-performing loans are at 0.03% which is the lowest among all commercial banks. This bank has been able to maintain the lower NPL in all past 5 years which indicates that the quality of the lending has been very good.

- Dividend History:

The bank has been providing a consistent dividend to the shareholders ranging from 14% to 21%. After the capital requirement of Rs. 8 Arab was reached in a previous year, the bank declared a 14% cash dividend to the shareholders this year.

- Branches & Staffs:

The bank has been expanding at a steady pace. With the increase in branches and staff, there is a challenge for the bank to increase its deposits which seems difficult looking at the current banking crisis.

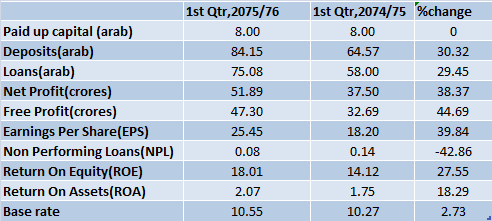

Financial Highlights: 1st Qtr 2075/76

The 1st quarter of this fiscal year for Sanima Bank seems promising. The deposits and loans grew by almost 30% from the previous year which is encouraging despite the credit crisis that is seen in this period. Net profit and free profit grew by an astounding 38% and 45% respectively. Due to this, EPS increased by 40 percent to Rs. 25.45. The ROE and ROA stand at 18.01 and 2.07 which are 28% and 18% higher than the previous year. The bank has continued to maintain its NPL at the low level which is at 0.08%, 43% less than the previous year. The base rate has increased slightly by 2.73% to 10.55

Future Prospects and challenges

The management seems capable to grow the business at a steady pace. Despite the current turmoil in the industry and heavy competition among banks, Sanima has shown impressive results in the first three months in this fiscal year. The management team has done a good job in the past to bring the bank at this level so quickly. And we can trust and believe that they will continue to do so in the future.

However, first of all, the current serious problems have to be dealt with to predict the rosy future for the bank. The aggressive attitude seen among banks has created difficulty to maintain the sanity and stick to basic principles of banking as a long-term business. The recent rise in deposit interest rate by other banks to as high as 13% will force the bank into one of the two situations: lose business to other banks or increase the deposit rate thereby doing business at a higher cost. The current scenario for the bank is to choose the bad among the worst. Also, it will be challenging for the bank to attract good clients for credit by lending them at a higher interest rate of 15-16%. To contain the default rate and NPL at low levels, as the bank has done in the past, seems to be difficult in the future.

Decision

The decision to invest in shares of Sanima bank lies solely in the nature of the individual. If you are a short-term investor, you will likely do well if you avoid this. The continuously depressive stock market, the recurring credit crunch and higher interest rates in the banking industry have hit the entire share market. The market recovery seems like a distant dream.

On the other hand, if you are a long-term investor and do not concern yourself with the current predicament, then Sanima bank is a good company to include in your portfolio. If you can see beyond the current clouds of uncertainty and hold the shares for the long run, you will be able to reap the rewards that this promising company will offer you in the future.

(Investments are subject to market risks and investors are advised to do personal homework before making any investment decision. This material is just a guideline for the investors to do further investigations)