Chhimek V/s Nirdhan Utthan Laghubitta: An Exclusive comparative study

May 5, 2019 | Investopaper

Chhimek Laghubitta and Nirdhan Utthan Laghubitta are the two leading microfinance of Nepal. This two microfinance are way ahead from other retail microfinance in terms of financial condition, profitability, business growth, and customer base. However, there is intense competition between the two that is going on for several years in the microfinance sector.

Chhimek and Nirdhan Utthan Laghubitta possess similar financial condition with neck to neck competition in business growth. Let us analysis the competitive position of this two microfinance based on the past and present fundamentals. We will divide the analysis into 4 major headings which are important from the point of view of investors. It includes the growth of loans and advances, growth of net profit, dividend paid to the shareholders and the current financial position until the third quarter of 2075/76.

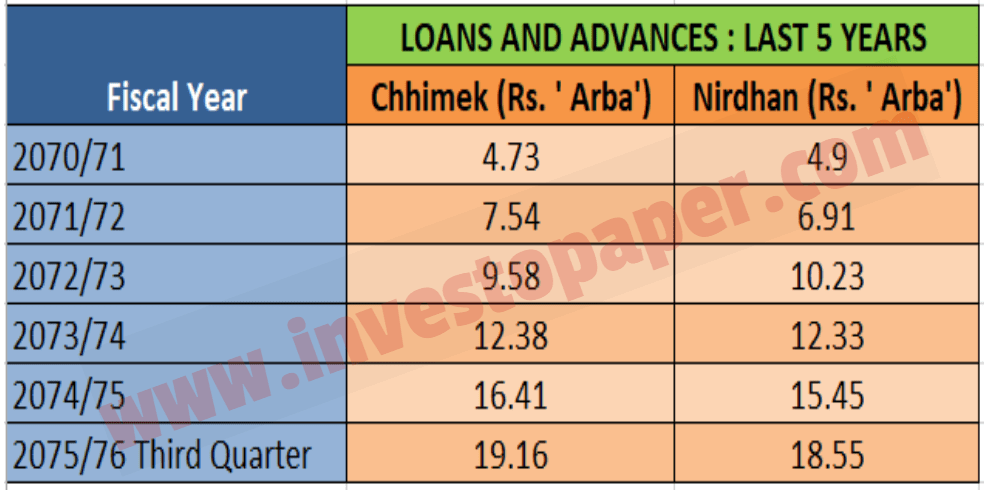

CHHIMEK V/S NIRDHAN UTTHAN: LOANS AND ADVANCES ( LAST 5 YEARS)

Chhimek and Nirdhan Utthan Laghubitta have grown their loans portfolio at an excellent rate. The loans have increased by almost 4 times in a period from 2070/71 to third quarter of 2075/76. Chhimek Laghubitta is able to increase the loans and advances from Rs. 4.73 Arba in 2070/71 to Rs.19.16 Arba in the third quarter of 2075/76. Similarly, Nirdhan Utthan increased its loans from Rs. 4.90 Arba to Rs. 18.55.

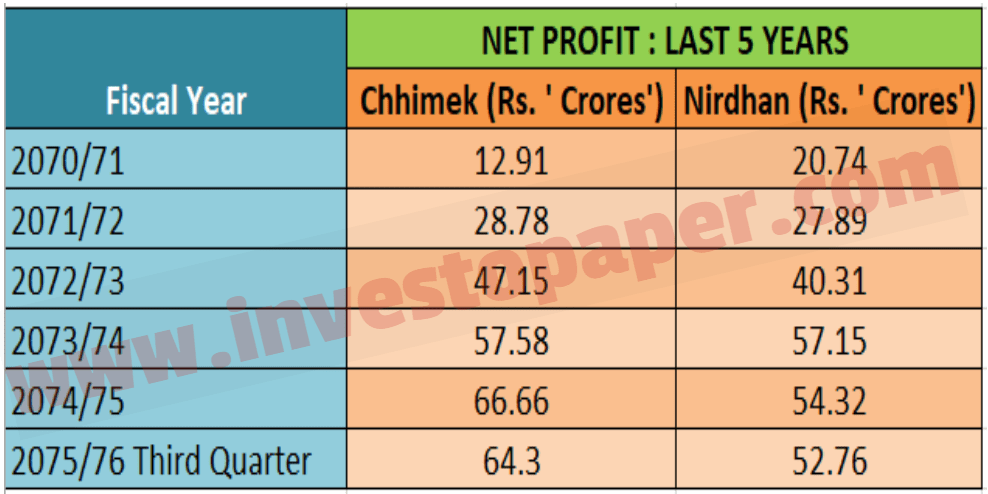

CHHIMEK V/S NIRDHAN UTTHAN: NET PROFIT ( LAST 5 YEARS)

Both the microfinance are highly profitable during the last 5 years period. Chhimek Laghubitta has increased the profit by almost 5 times during this period while Nirdhan Utthan almost tripled its profit. The profit of Chhimek Laghubitta has grown from Rs. 12.91 crores in F.Y. 2070/71 to Rs. 66.66 crores in the 2074/75. Until the third quarter of 2075/76, the company has made Rs. 64.30 crores in profit. The profit is expected to cross Rs. 85 crores in this fiscal year.

On the other hand, Nirdhan Utthan Laghubitta has improved its profit from Rs. 20.74 crores in 2070/71 to Rs. 54.32 crores in 2074/75. The microfinance made a profit of Rs. 52.76 crores until the third quarter. The profit is estimated to rise to above Rs. 70 crores at the end of this fiscal year.

In fiscal year 2073/74 both microfinance were equally profitable with Rs. 57 crores in net profit. However, after that period due to the increase in the cost of fund led by the credit crisis in the economy, Nirdhan Utthan is lagging behind in growth. Chhimek looks more aggressive than Nirdhan Utthan in its profit growth in the last couple of years.

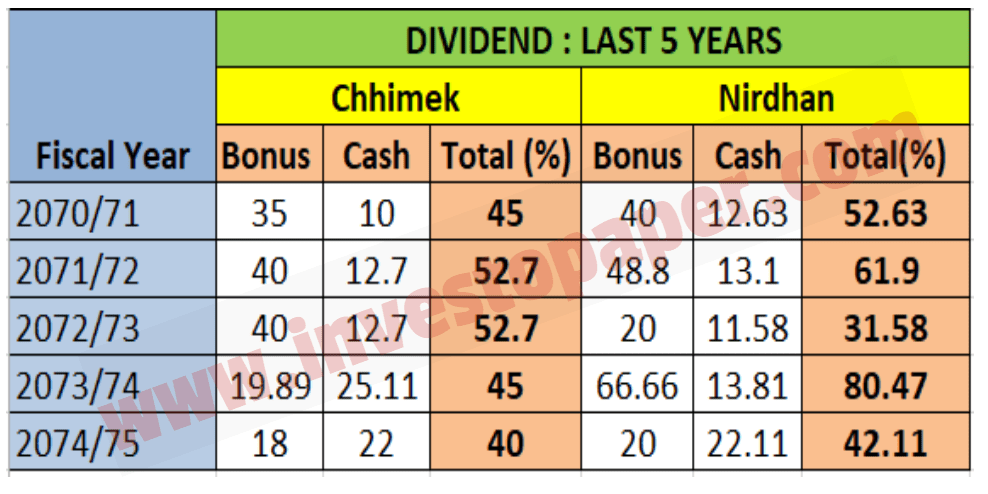

CHHIMEK V/S NIRDHAN UTTHAN: DIVIDEND ( LAST 5 YEARS)

The dividends distributed by both the microfinance in the last 5 years is highly satisfactory to the shareholders. They have focused mainly on bonus shares which are more favored by Nepalese investors. Chhimek Laghubitta has distributed dividend ranging from 40 percent to almost 53 percent. On the other hand, Nirdhan Utthan has provided dividend ranging from 32 percent to 81 percent during these five years.

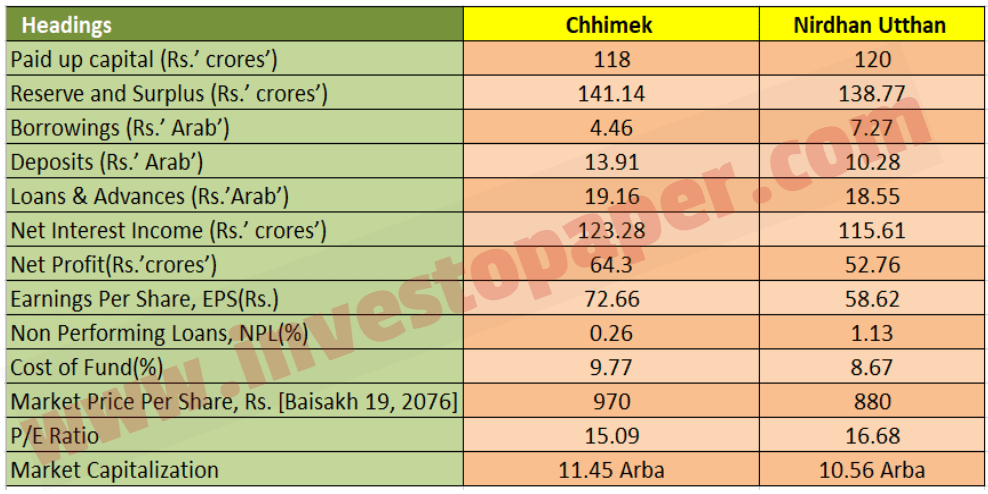

CHHIMEK V/S NIRDHAN UTTHAN: FINANCIAL HIGHLIGHTS, 3RD QUARTER, 2075/76

Based on the third-quarter report of 2075/76, Chhimek Laghubitta has Rs. 118 crores in the capital with Rs. 141 crores in reserves and surplus. On the other hand, Nirdhan Utthan Laghubitta has Rs. 120 crores in the capital with Rs. 139 crores in reserves. The loans and advances of Chhimek and Nirdhan Utthan stand at Rs. 19.16 Arba and Rs. 18.55 Arba respectively. In terms of EPS, Chhimek has left Nirdhan Uthan behind by Rs. 14 per share. Chhimek and Nirdhan Utthan EPS stand at Rs. 72.66 and Rs. 58.62 crores respectively until the third quarter.

The market capitalization of Chhimek Laghubitta (based on the market price of Baisakh 19, 2076) is Rs. 11.45 Arba. While Nirdhan Utthan Market capitalization stands at Rs. 10.56 Arba. This indicates that investors are valuing Chhimek more than Nirdhan Utthan in the current market. This is justifiable looking at the current performance of Chhimek. Choosing one(Chhimek) among the two may look easy looking at the current trend. However, neglecting the other (Nirdhan Utthan) may cause regret to the investors due to its probability of bouncing back and claiming itself as the number one microfinance.

Investors won’t go wrong if they include both the microfinance in their portfolio instead of one, dividing the money into two in the ratio they prefer. Both microfinance will continue to lead in the coming days in their sector unless any catastrophic decisions or situations come into play.

CBBL is better than NUBL

कृपया 100000लगानीको १०बर्षमा कति होला

Minimum 6 lakh hunchha