Comprehensive Study on Interest Rate in Nepal: Structure, Trends, & Volatility

December 12, 2025 | Investopaper

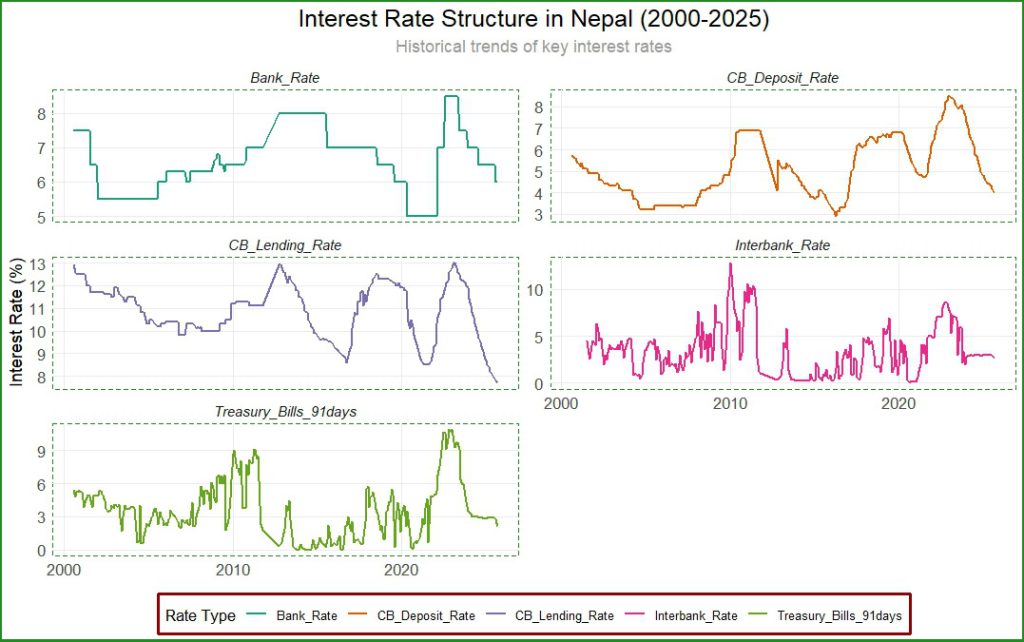

Interest rates play a crucial role in any economy, influencing investment decisions, consumption patterns, inflation, and overall economic growth. In Nepal, the Nepal Rastra Bank (NRB) uses various monetary policy tools, with the Bank Rate being a key instrument to signal its policy stance. This study presents a detailed analysis of the structure and trends of interest rates in Nepal from August 2000 to September 2025. It examines key interest rate indicators including the Bank Rate (policy rate), Treasury Bills (91-day), Interbank Rate, Commercial Banks’ Deposit and Lending Rates, and the resulting Interest Rate Spread. The analysis reveals significant shifts in Nepal’s interest rate environment over the past 25 years, with notable periods of monetary tightening and easing, changing spreads, and varying levels of volatility.

Methodology

The studyutilizes monthly data from August 2000 to September 2025. The following interest rate indicators were examined:

Bank Rate: The policy rate set by Nepal Rastra Bank

Treasury Bills (91 days): Short-term government securities rate

Interbank Rate: Rate at which banks lend to each other

Commercial Banks’ Deposit Rate: Average rate offered by commercial banks on deposits

Commercial Banks’ Lending Rate: Average rate charged by commercial banks on loans

Interest Spread: Difference between lending and deposit rates

Statistical methods included descriptive statistics, correlation analysis, and visualization techniques such as time series plots, distribution analysis, and volatility measurements using 12-month rolling standard deviations.

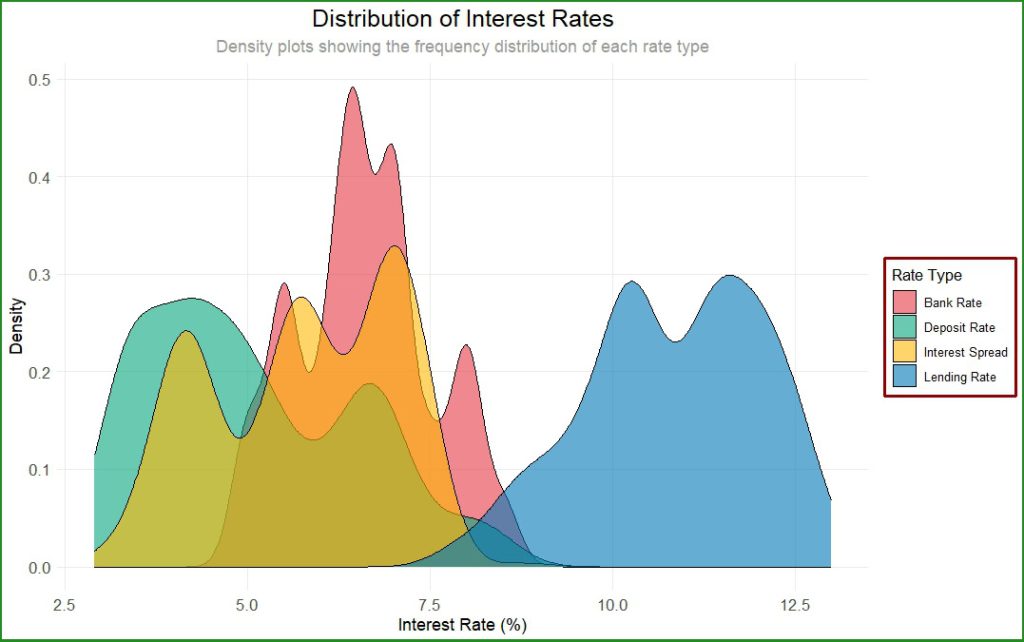

Descriptive Statistics

Summary of Interest Rate Indicators (2000-2025)

| Indicator | Mean | Median | Min | Max | Latest (Sep 2025) |

|---|---|---|---|---|---|

| Bank Rate (Policy Rate) | 6.60% | 6.50% | 5.0% | 8.5% | 6.0% |

| 91-day Treasury Bill Rate | 3.57% | 3.20% | 0.0% | 10.9% | 2.1% |

| Interbank Rate | 3.44% | 3.00% | 0.0% | 12.8% | 2.7% |

| Commercial Bank Deposit Rate | 5.07% | 4.80% | 2.9% | 8.5% | 4.0% |

| Commercial Bank Lending Rate | 10.83% | 11.10% | 7.7% | 13.0% | 7.7% |

| Interest Rate Spread | 5.76% | 5.80% | 3.0% | 8.8% | 3.7% |

Long-term Trends and Key Phases

| Period | Characteristics | Remarks |

|---|---|---|

| 2000 – 2007 | High and stable policy & lending rates (12–13%), moderate spreads (~6–7%) | Post-conflict recovery, limited liquidity |

| 2008 – 2011 | First major liquidity crisis (2008–09), short-term rates spiked to 12–13% | Remittance-fueled credit boom |

| 2012 – 2015 | Extremely wide spreads (peaked 8.8% in 2012), persistent excess demand for credit | Slow deposit growth |

| 2016 – 2019 | Gradual normalization; spreads began narrowing as NRB reduces spread rates. | Earthquake reconstruction, hydropower lending |

| 2020 – mid-2021 | COVID-19 liquidity glut → T-bill & interbank rates near 0%, lending rates fell sharply | NRB moratoriums, huge liquidity injection |

| 2022 – 2023 | Severe liquidity crunch → Bank Rate hiked to 8.5%, lending rates touched 13%, highest volatility | Import restrictions, declining remittances, reserve crisis |

| 2024 – 2025 | Rapid easing cycle → Policy rate cut from 8.5% → 6.0%, lending rates collapsed to ~7.7% | Liquidity normalization, easing of import curbs |

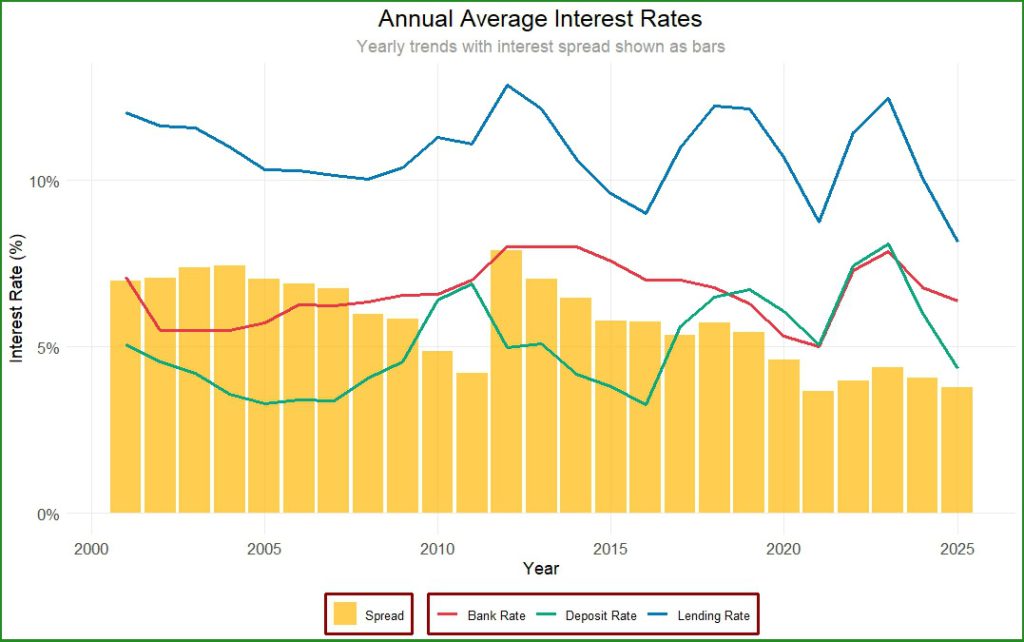

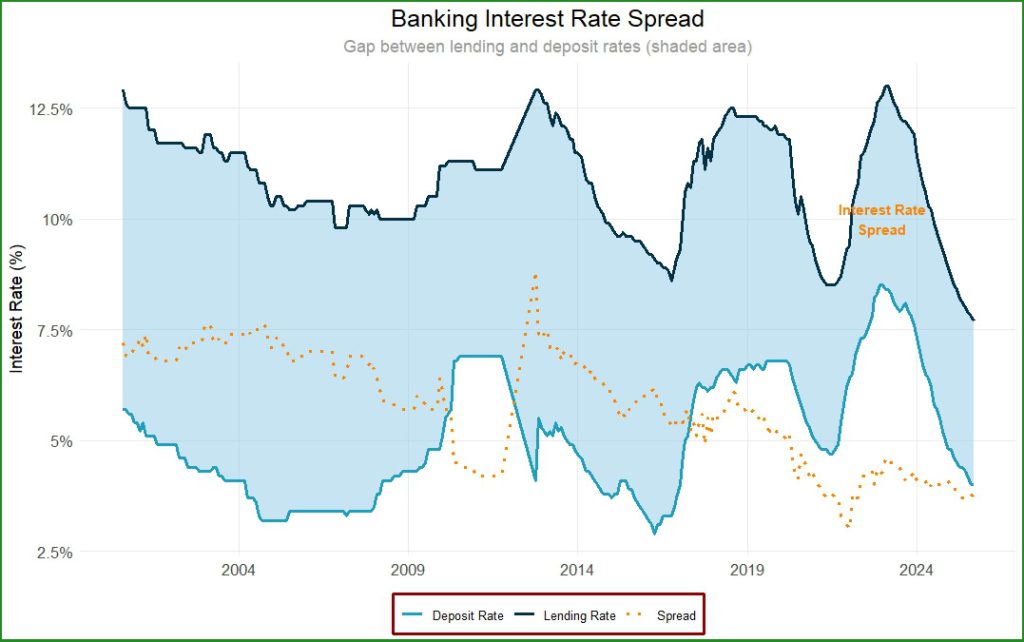

Interest Rate Spread

The interest rate spread is the difference between the lending and deposit rates offered by the banks and financial institutions.

From a chronically high 7–8%+ for most of 2000–2015, the spread has fallen to 3.7% in 2025.

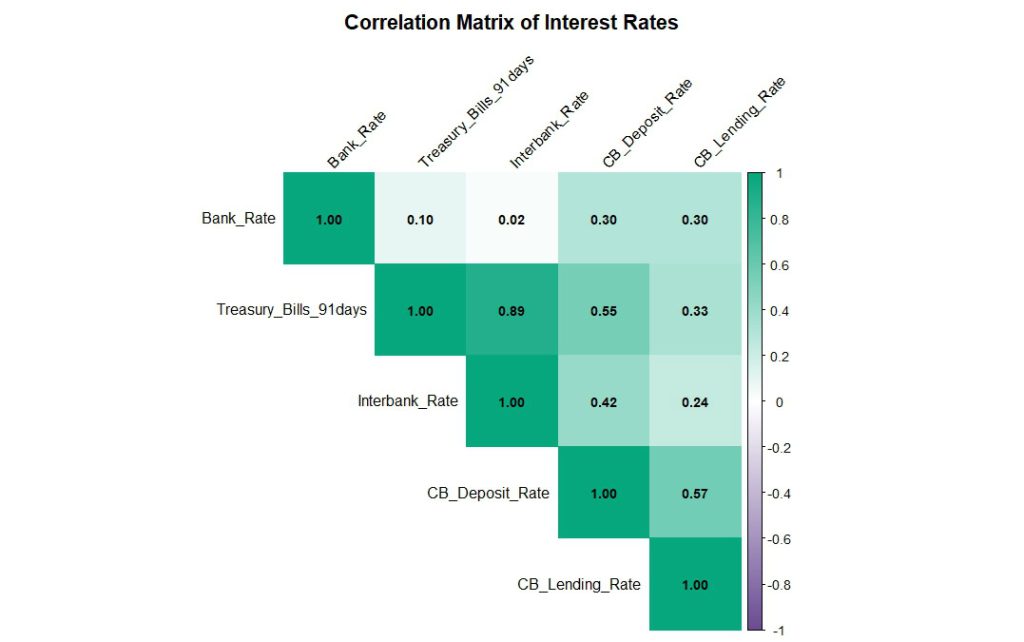

Correlation Analysis

| Bank Rate | T-Bill 91d | Interbank | Deposit Rate | Lending Rate | |

|---|---|---|---|---|---|

| Bank Rate | 1.000 | 0.097 | 0.021 | 0.303 | 0.301 |

| 91-day T-Bill | 1.000 | 0.889 | 0.547 | 0.333 | |

| Interbank Rate | 1.000 | 0.420 | 0.236 | ||

| Commercial Bank Deposit | 1.000 | 0.569 | |||

| Commercial Bank Lending | 1.000 |

Key takeaways:

Short-term market rates (T-bill & interbank) are very highly correlated (0.89) — expected.

Deposit and lending rates move together (0.57), confirming that spreads are relatively sticky.

Policy rate (Bank Rate) has surprisingly low correlation with market rates, suggesting the transmission mechanism is still imperfect and operates with long lags.

You May Also Like:

Comprehensive Analysis of Tourist Arrivals and Stay Patterns in Nepal

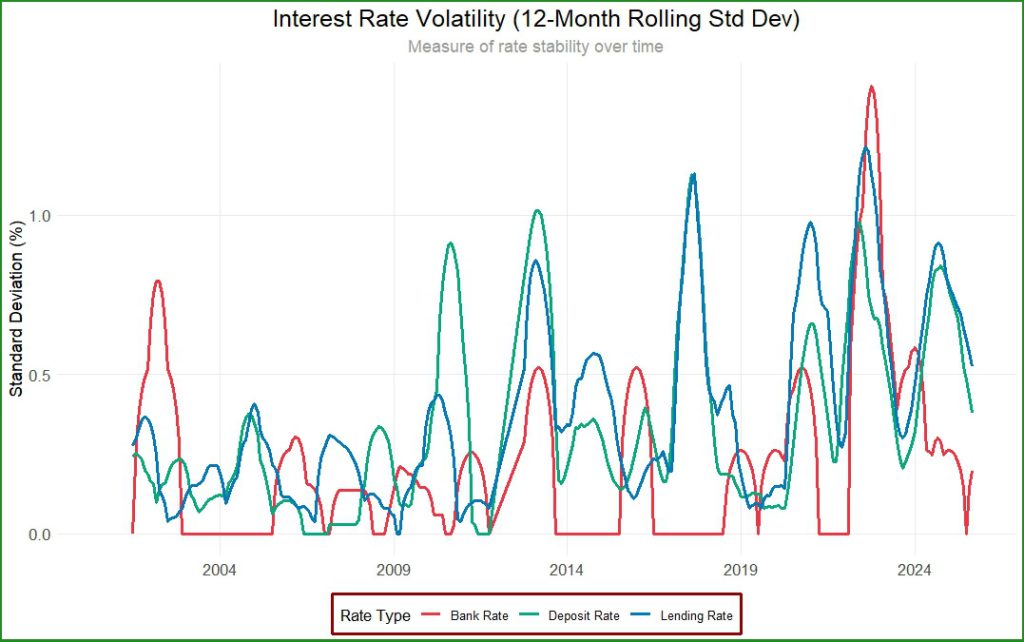

Volatility Patterns

The Bank Rate has shown the lowest volatility, reflecting its nature as a policy instrument that changes infrequently. In contrast, market-determined rates like Treasury Bills and Interbank Rates have exhibited higher volatility.

The 12-month rolling standard deviation analysis reveals several periods of heightened interest rate volatility:

2002-2003: Moderate volatility during a period of Bank Rate adjustments

2008-2009: Increased volatility during the global financial crisis

2010-2011: High volatility in Treasury Bills and Interbank Rates

2015-2016: Moderate volatility following the earthquake

2022-2023: Significant volatility across all rates during monetary tightening

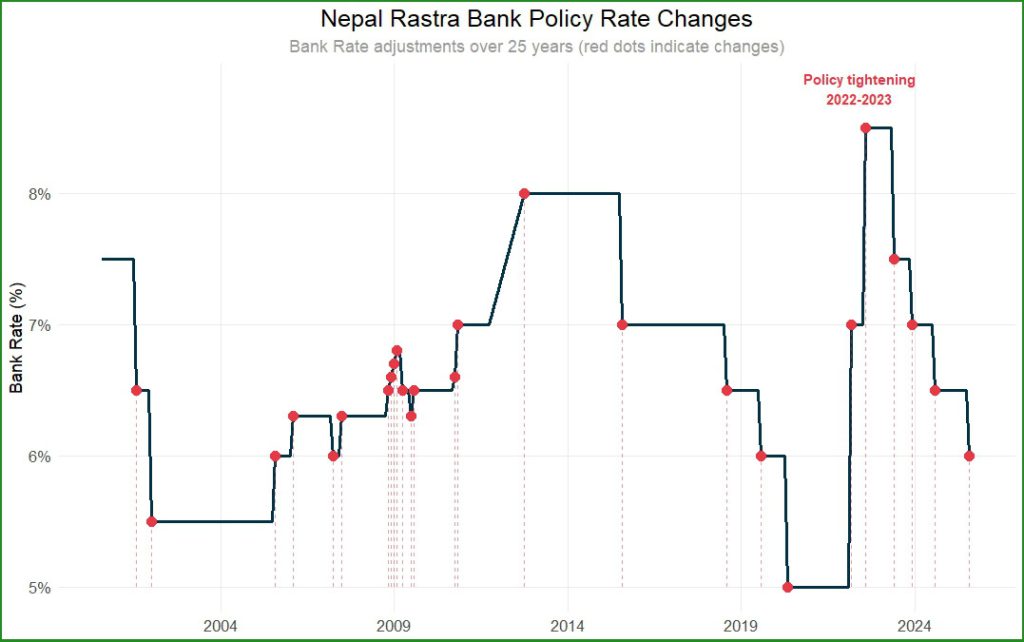

Policy Rate Changes

The analysis of Bank Rate changes reveals that Nepal Rastra Bank has adjusted its policy rate infrequently but significantly:

2001-2002: Gradual reduction from 7.5% to 5.5% (easing cycle)

2005-2008: Gradual increase to 6.5% (tightening cycle)

2012: Increase to 8.0% (further tightening)

2015: Reduction to 7.0% (easing)

2022: Sharp increase to 8.5% (aggressive tightening)

2023-2025: Gradual reduction to 6.0% (easing cycle)

Recent Trends (2020-2025)

The period from 2020 to 2025 has been particularly dynamic, featuring:

COVID-19 Impact (2020): Initial rate cuts to support the economy

Recovery Phase (2021): Gradual normalization of rates

Inflation Response (2022-2023): Aggressive tightening with Bank Rate rising to 8.5%

Stabilization (2023-2025): Gradual easing as inflationary pressures subsided

Conclusion

The interest rates in Nepal have witnessed higher fluctuations amid changes in the liquidity in the banking system. There have been several episodes of liquidity cruch in the system which have led to sharp rises in the interest rates. However, the interest rates have recovered to lower levels with rise in remittance income and NRB policy tightening. The spread between lending and deposit rates has also gradually narrowed over the last 25 years. In order to develop the financial and economic system, it is essential to manage the liquidity and interest rates at lower levels to foster investment and increase economic activities.

More From Investopaper:

A Study on NEPSE: Growth of Index, Market Cap, Listed Companies and Trading Turnover

From Scarcity to Surplus: Five Decades of Nepal’s Electricity Transformation